Most founders mess up post-money valuation because they treat it like simple arithmetic, then discover during Series A that they’ve accidentally given away 30% of their company instead of 20%. The math itself is straightforward—pre-money plus new investment equals post-money—but the devil is in what you include: option pools, convertible notes, SAFEs, and whether those instruments use pre-money or post-money caps.

This guide shows you exactly how to calculate post-money valuation in every scenario, explains common mistakes that destroy cap tables, and provides worked examples for priced rounds, SAFE conversions, and multi-instrument stacks. You’ll also get a simple framework to audit your cap table before signing any term sheet.

Table of Contents

- The basic post-money valuation formula

- Step-by-step calculation for priced equity rounds

- Post-money valuation with SAFEs and convertible notes

- How option pools affect post-money calculations

- Common mistakes and how to avoid them

- Cap table audit checklist before signing terms

- Frequently asked questions about post-money valuation

1. The basic post-money valuation formula

1.1 The simplest version

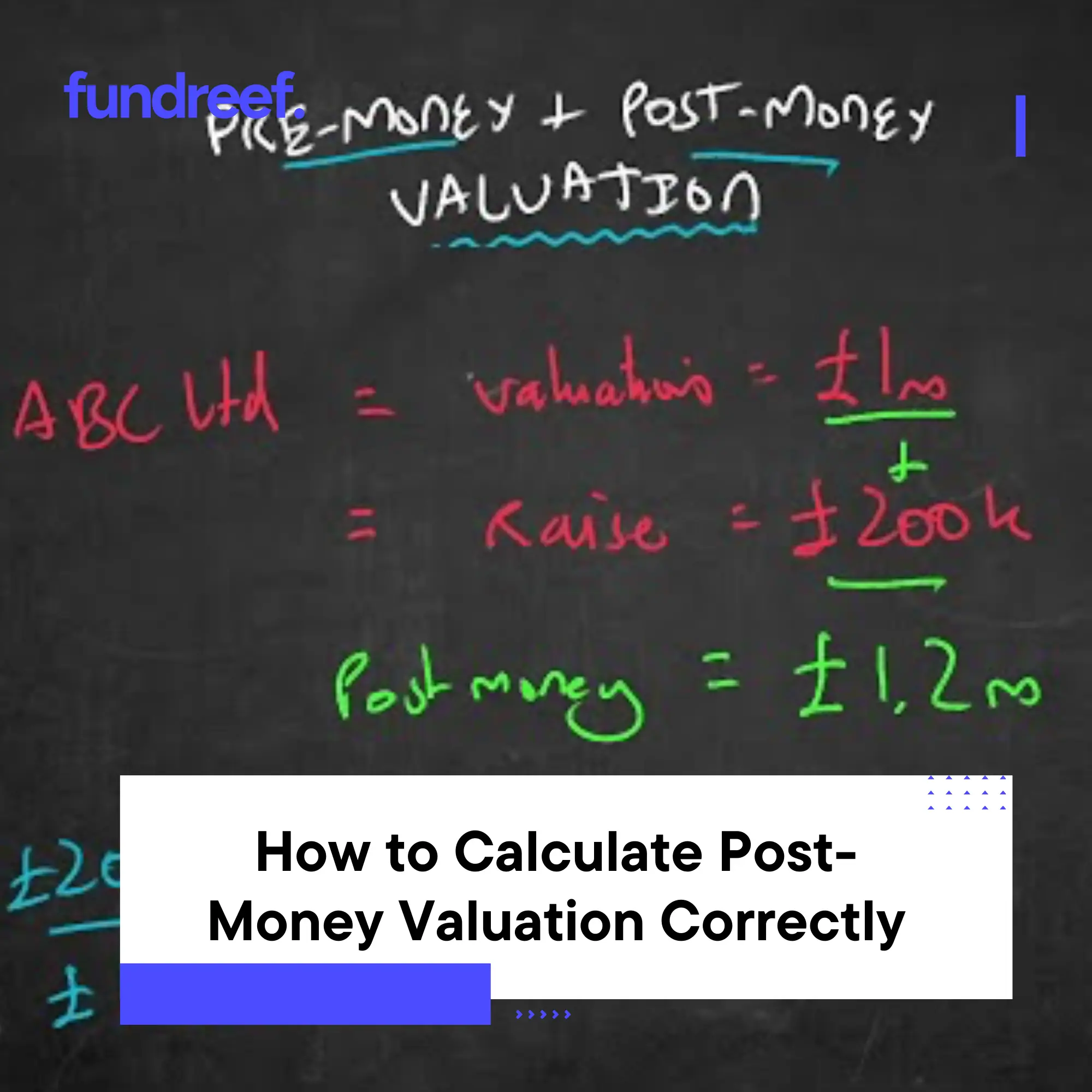

Post-money valuation is the value of your company immediately after new money comes in:

Post-money valuation=Pre-money valuation+New investment

Example: You raise $2M at $8M pre-money.

Post-money = $8M + $2M = $10M.

The investor now owns $2M / $10M = 20% of your company. You (and existing shareholders) own 80%.

1.2 Why this matters

Post-money determines ownership percentages. Investors care about post-money because it tells them exactly what slice of the company they’re buying. Founders care because it determines dilution.

If you negotiate “higher valuation” without clarifying pre vs post, you might accidentally agree to more dilution than you think.

2. Step-by-step calculation for priced equity rounds

2.1 Simple scenario: no option pool, no prior instruments

You’re raising a Series A. Clean cap table: founders own 100%, no SAFEs or notes outstanding.

Given:

- Pre-money valuation: $12M

- Investment amount: $3M

Step 1: Calculate post-money valuation.

Post-money=$12M+$3M=$15M

Step 2: Calculate investor ownership.

Investor %=$15M$3M=20%

Step 3: Calculate founder dilution.

Founders owned 100%, now own 80%.

2.2 With an option pool expansion

VCs often require option pool expansion pre-money, which changes the math.

Given:

- Pre-money valuation: $12M

- Investment: $3M

- VCs want a 15% option pool (currently only 5%)

Step 1: Expand option pool before the round.

Adding 10% more options dilutes only founders:

Effective pre-money = $12M × (1 – 0.10) = $10.8M (founders’ share)

Total pre-money still $12M, but founders now own ~90% pre-money instead of 100%.

Step 2: Calculate post-money.

Post-money=$12M+$3M=$15M

Step 3: Calculate ownership.

Investor: $3M / $15M = 20%

Option pool: 15%

Founders: 65% (diluted by both the round and pool expansion)

Key insight: Always clarify whether option pool expansion happens pre or post-money. Pre-money expansion dilutes founders more.

2.3 Alternative formula using investor ownership

If you know the investor’s desired ownership percentage and investment amount, you can work backward:

Post-money valuation=Investor ownership %Investment amount

Example: Investor wants 20% for $3M.

Post-money=0.20$3M=$15M

Pre-money=$15M−$3M=$12M

This is useful when negotiating: if an investor says “we want 25%,” you can immediately calculate what pre-money that implies for any given check size.

3. Post-money valuation with SAFEs and convertible notes

3.1 Pre-money SAFEs (original YC template)

With pre-money SAFEs, the valuation cap is applied before counting other SAFEs. This means later SAFEs dilute earlier SAFE holders and founders.

Example: Two $500k SAFEs, both at $5M pre-money cap.

When they convert at Series A ($10M pre-money), here’s the math:

Step 1: Calculate conversion price for each SAFE.

First SAFE: $5M cap → converts at $5M pre (before second SAFE).

Second SAFE: Also converts at $5M cap (before counting itself).

Step 2: Total shares issued.

This gets complex because SAFEs dilute each other. Simplified:

Total dilution ≈ $1M / $5M = ~20% (split between both SAFEs plus founders).

Pre-money SAFEs are founder-friendlier when stacking multiple instruments but harder to model precisely without cap table software.

3.2 Post-money SAFEs (YC 2018+ template)

Post-money SAFEs are simpler: the cap includes all SAFEs. Each SAFE locks in its ownership percentage at conversion.

Example: Two $500k SAFEs at $5M post-money cap.

Step 1: Calculate ownership per SAFE.

SAFE 1: $500k / $5M = 10%

SAFE 2: $500k / $5M = 10%

Total SAFE dilution: 20%

Step 2: At Series A conversion, founders own 80% (pre-Series A money).

Step 3: Series A investment ($3M at $12M pre) further dilutes everyone.

Post-money after Series A:

Post-money=$12M+$3M=$15M

Series A investor: 20%

SAFEs (collectively): 20% × 0.80 = 16% (diluted by Series A)

Founders: 64%

Key difference: Post-money SAFEs are more investor-friendly (predictable ownership) but more dilutive to founders when stacking multiple instruments.

3.3 Convertible notes with interest

Convertible notes accrue interest, so the principal grows over time.

Example: $200k note at 8% annual interest, 18-month term.

Interest accrued: $200k × 0.08 × 1.5 = $24k

Total principal at conversion: $224k

If the note has a $5M cap and 20% discount, you calculate conversion using the lower of:

- Cap-based price

- Discount-based price

Then divide $224k by that price to determine shares issued.

Always model notes with accrued interest to avoid cap table surprises.

4. How option pools affect post-money calculations

4.1 Pre-money vs post-money pool expansion

Pre-money pool expansion (investor-friendly):

Pool created before valuation, dilutes only existing shareholders (founders).

Post-money pool expansion (founder-friendly, rare):

Pool created after valuation, dilutes everyone including new investors.

Example comparison:

| Scenario | Pre-money pool | Post-money pool |

|---|---|---|

| Pre-money valuation | $10M | $10M |

| Investment | $2M | $2M |

| Pool size | 15% | 15% |

| Post-money valuation | $12M | $12M |

| Investor ownership | 16.67% | ~14.3% |

| Founder ownership (after pool & round) | 68.33% | ~70.7% |

VCs almost always demand pre-money pool expansion. If you can negotiate post-money (rare), it saves you 2–3% dilution.

4.2 Fully diluted vs non-diluted calculations

Always use fully diluted capitalization (includes all options, warrants, SAFEs, notes) when calculating post-money valuation and ownership percentages.

Non-diluted numbers (common shares only) are misleading and will confuse investors during diligence.

5. Common mistakes and how to avoid them

5.1 Confusing pre and post-money in conversation

Mistake: Investor says “$10M valuation,” you assume pre-money, they meant post-money. You think you’re giving 20%, but it’s actually 25%.

Fix: Always clarify explicitly: “Is that $10M pre-money or post-money?”

5.2 Ignoring SAFE stacking dilution

Mistake: You raise three $200k SAFEs at $5M post-money cap, thinking total dilution is 12% ($600k / $5M). But each SAFE independently locks 4%, so total dilution is actually closer to 12% per SAFE, compounding to higher dilution.

Fix: Model every SAFE individually with cap table software (Carta, Pulley, Capboard). Don’t do napkin math with multiple post-money SAFEs.

5.3 Forgetting accrued interest on notes

Mistake: You raise $500k on a convertible note, forget about 8% annual interest for 2 years. At conversion, principal is actually $580k, not $500k—extra shares issued you didn’t expect.

Fix: Always calculate accrued interest through the expected conversion date and include it in cap table projections.

5.4 Option pool timing games

Mistake: VCs say “15% pool post-money,” but the term sheet actually says “15% pool created pre-money.” You don’t catch it, and you dilute 3–5% more than expected.

Fix: Read the exact language in the term sheet. If it says “pool to be X% of post-money capitalization,” that usuallymeans pre-money creation (confusing but standard). Ask your lawyer to confirm.

5.5 Using old cap tables

Mistake: You raised a SAFE 9 months ago, never updated your cap table, now raising Series A and realize you have no clean view of current ownership.

Fix: Update your cap table after every transaction (SAFE, note, option grant, equity sale). Use cap table software, not spreadsheets.

When you’re preparing for a fundraise and need to present clean dilution scenarios to potential investors, platforms like Fundreef can help you identify VCs who understand complex cap table structures—filter for funds that have backed companies with SAFE stacks or messy early rounds, so you’re pitching investors who won’t freak out during diligence and know how to model these correctly.

6. Cap table audit checklist before signing terms

Before you sign any term sheet, run through this checklist:

- Do I know the exact pre-money and post-money valuations?

- Is the option pool expansion pre or post-money?

- What percentage of the company will investors own post-close?

- What percentage will founders own after this round?

- Have I modeled all outstanding SAFEs, notes, and warrants?

- Have I included accrued interest on convertible notes?

- Is my cap table fully diluted (includes all future conversions)?

- Have I run scenarios for the next round (Series A → Series B)?

- Does my lawyer agree with my cap table math?

- Do I have written confirmation of pre vs post from the investor?

If you answer “no” or “I’m not sure” to any of these, stop and fix it before signing.

Frequently asked questions about post-money valuation

What is the formula for post-money valuation?

Post-money valuation = Pre-money valuation + New investment. For example, if you raise $3M at $12M pre-money, post-money is $15M. Alternatively, if you know investor ownership, post-money = Investment ÷ Investor ownership % (e.g., $3M ÷ 20% = $15M).

How do I calculate investor ownership from post-money valuation?

Investor ownership % = New investment ÷ Post-money valuation. Example: $2M investment at $10M post-money = 20% investor ownership. Founders are diluted from 100% to 80%.

What’s the difference between pre-money and post-money valuation?

Pre-money is your company’s value before new investment. Post-money is the value after new money is added. Post-money = Pre-money + Investment. Post-money determines ownership percentages; pre-money is often what founders negotiate.

How does option pool expansion affect post-money valuation?

If the pool expands pre-money (standard), it dilutes founders before the new investment, effectively lowering the true pre-money value for founders. If the pool expands post-money (rare), everyone including new investors gets diluted. Always clarify timing in the term sheet.

Do SAFEs use pre-money or post-money valuation?

Depends on the SAFE version. Pre-money SAFEs (original YC) apply the cap before counting other SAFEs, so later SAFEs dilute earlier ones. Post-money SAFEs (YC 2018+) include all SAFEs in the cap, giving each SAFE a predictable ownership percentage but increasing total founder dilution when stacking multiple SAFEs.

How do I avoid mistakes when calculating post-money valuation?

Always clarify pre vs post explicitly with investors. Use fully diluted capitalization (include all SAFEs, notes, options). Model accrued interest on convertible notes. Update your cap table after every transaction. Use cap table software (Carta, Pulley) instead of spreadsheets. Get lawyer confirmation before signing term sheets.

Suggested visuals to create

- Post-money calculation flowchart

Decision tree: “Do you have SAFEs/notes?” → Yes/No → “Pre-money or post-money SAFEs?” → Step-by-step calculation paths for each scenario. - Dilution comparison table

Side-by-side showing founder ownership after same $3M raise at different structures: clean round, with pre-money pool, with post-money SAFEs, with stacked notes. - Cap table evolution example

Visual showing ownership % progression across three funding events: Seed (SAFEs) → Series A (priced + pool) → Series B (priced), with dilution at each step.